The key to capital structure strategy is balancing risk and reward.

Companies commonly finance acquisitions, growth capital, recapitalizations and other business expenditures with external funding sources, rather than relying solely on internal cash flows. Savvier financial leaders adhere to the strategy of tactically optimizing their company’s capital structure to support both short-term and long-term business plans, making ongoing adjustments as needed. Thoughtfully balancing risk (added leverage) with reward (faster growth, accomplishing other business or ownership goals) can provide greater opportunity to maximize ROI.

Learning about the benefits and drawbacks of diverse types of capital, combined with understanding the total potential availability of capital under various scenarios, enables management to improve strategic planning at the board level as well as create or quickly respond to opportunities, such as the pursuit of an attractive acquisition target.

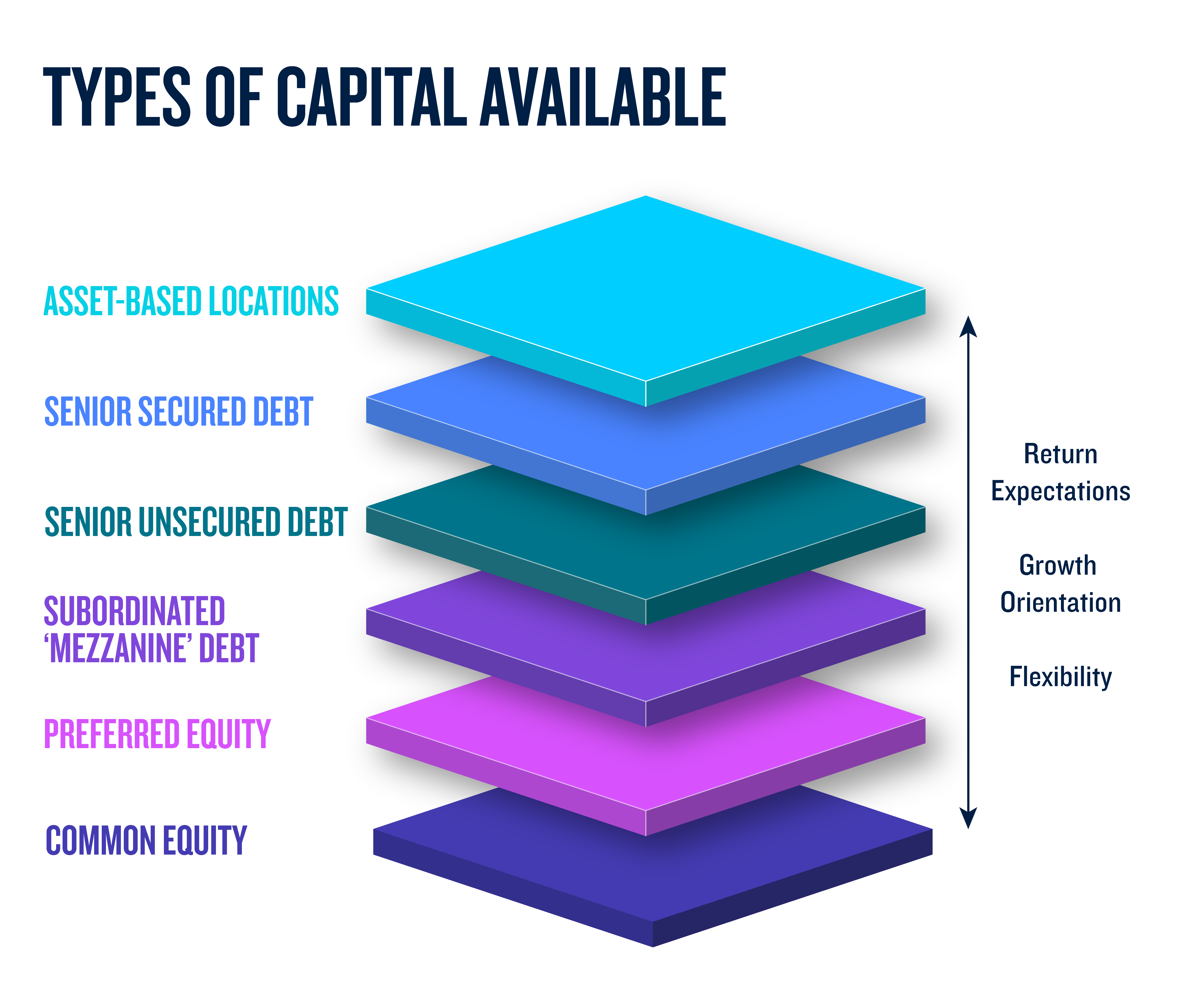

The image below depicts the common types of capital available to companies, shown in order of payback priority (with highest priority on top). As a rule, capital with higher payback priority has lower risk, and therefore, lower return expectations to the investor as well as cost to the company. Capital with lower payback priority has higher risk, and therefore, higher return expectations for the investor and cost to the company.

A Comparison of the Types of Capital Available

- Asset-Based Loans — These secured, traditional senior debt loans come in two flavors; the first is a ‘loan-to-value’ note secured by specific plants/facilities or equipment, based on appraisal (commonly referred to as equipment financing). The second is formula-driven and based on metrics, such as the amount of working capital and receivables held by a business. In terms of cost of capital, asset-based loans have the advantage of being relatively less expensive. However, in terms of the amount of capital that can be raised, they are limited by the assets they are based on.

- Senior Secured Debt: Secured asset-based senior traditional bank loans — Another type of senior debt is a loan on offer by local, regional and national banks that provide negotiated amounts of capital, secured by a blanket lien on the business. These loans have the advantage of offering potentially more capital than an asset-based loan, potentially at a slightly higher cost.

- Senior Unsecured Debt: Unsecured cash-flow-based senior traditional bank loans — Once a middle-market company demonstrates meaningful scale and stability over a long period of time, they may graduate from secured asset-based loans to unsecured cash-flow based facilities. Regional and national banks will provide negotiated amounts of capital without placing a blanket lien on the business. These loans are typically governed by financial covenants based on earnings, and will provide additional flexibility for the business, compared to a senior secured financing.

"Mezzanine is the last stop along the capital structure where owners can raise large amounts of liquidity without selling a stake in their company."

- Subordinated ‘Mezzanine’ Debt — As the name implies, this type of financing is a hybrid of senior debt and equity. Mezzanine debt is typically unsecured and subordinate in terms of payback priority to any senior debt. Because of the greater risk taken by the investor, mezzanine is more costly than senior debt, but less expensive than equity. Mezzanine is also typically more ‘patient’ than senior financing, with no required amortization before maturity as well as a longer dated final maturity than senior debt.

Additionally, mezzanine is the last stop along the capital structure where owners can raise large amounts of liquidity without selling a stake in their company. Most companies utilize mezzanine financing to accomplish a specific goal, such as a significant acquisition or ownership transfer by completing a mezzanine-supported recapitalization, or ‘minority recapitalization,’ and transition to a more conservative capital structure over time.

- Preferred Equity — For those companies that require capital and are open to involvement from an outside investor, selling an equity stake in the company is an option. Such a transaction is typically completed by a private equity fund or institutional investor, where capital is exchanged for equity ownership. Preferred equity offers investors greater downside protection through ‘debt-like’ features, such as a liquidation preference (higher ‘first out’ position than common stock) as well as a mandatory dividend. In exchange for downside protection, the preferred equity investor will take a lower share of the ownership, allowing existing shareholders to retain a higher percentage of ownership, thereby increasing their potential returns and retaining governance control of the business.

- Common Equity — Like preferred equity, common equity also involves selling an equity share of the business and is typically funded by a private equity fund or institutional investor. However, given the greater amount of risk, common equity investors have slightly higher return requirements than preferred equity investors, and they often require a majority, or control, position.

Overview of Capital Structuring

A company’s capital structure should be optimized to fit the long-term vision for the business as well as position the company to take advantage of investment opportunities that could arise 3-5 years down the road. Companies that adopt this mindset will implement a capital structure strategy that reserves borrowing capacity for large or near-term expenditures and preserves capital structure flexibility.

The appropriate capital structure for a company fluctuates depending on their overall strategy, the market environment, the competitive environment as well as their short-term (3-5-year) strategic business plan.

As mentioned earlier, the hierarchy of a capital structure is based on payback priority; senior layers would be paid first, then mezzanine, with equity paid last. A typical capital structure utilizing this combination of capital might look like the following:

Leverage

When determining how much debt or leverage to take on in terms of the risk/reward spectrum, companies should ask themselves the following questions:

- How much debt capacity can my company service?

- How much risk am I willing to put on my business?

For a company to implement the capital structure above, they most likely would have maximized their senior debt borrowing capacity or are trying to preserve future senior debt capacity by adding a temporary layer of mezzanine debt to be used for a specific purpose.

In determining how companies can structure their balance sheets to maximize returns and balance risks, general qualitative factors include:

- Operating Leverage – Defined as the level of fixed costs in a business model; the higher the fixed-cost base, the higher the risk (i.e. variable earnings). Pairing high operational fixed costs with high leverage increases risk.

- Cyclicality – Defined as the normal variation of demand experienced by a business (vs. seasonality). Pairing highly variable earnings with high leverage increases risk.

- Concentration – Defined as a significant portion of revenue/earnings derived from a customer, product, location or operation. Pairing highly concentrated businesses with high leverage increases risk.

With regards to making decisions on capital structure and leverage, financial leaders are also faced with balancing conflicting objectives of corporate constituents, juggling the goals of the company, the shareholders as well as debtholders:

Capital Structure Strategy Example

The Jones family started the transportation services company, XL Transport, Inc. many years ago. They are interested in buying out their biggest competitor, Large Freight. The acquisition is a great strategic opportunity for XL Transport, but the Joneses don’t want to sell equity in the company to complete the purchase. Alternatively, they can use mezzanine capital to fund the transaction, while maximizing shareholder value.

So, the Joneses can either make the acquisition of Large Freight with capital structure Option A (Sell Equity Interest) or capital structure Option B (Utilize Mezzanine). Let’s see how this plays out:

As you can see, with Option A, the Joneses had to forgo 33% ownership stake of the business when they made the equity sale. However, with Option B, where the Joneses utilized mezzanine financing, they only gave up 2% ownership stake, and the value of their holdings was only $1.8 million less than the value of their final holdings for Option A.

Now, let’s look at the performance of XL Transport five years later:

When developing a capital structure strategy, it’s in the interest of the financial leaders of a company to familiarize themselves with the types of capital available to make more tactical decisions about their company’s capital structure, better positioning them to accomplish both short-term and long-term goals.

It may be difficult to determine which types of capital to utilize at a given time, PGIM can help you navigate the options as well as customize a financing solution that can enable your business to reach that coveted balance of risk and reward.